#12: What kind of business has Viking built?

One of travel's most successful companies files to go public and reveals their numbers. The filing is 200+ pages. I read it so you didn't have to.

Friday was exciting: Viking Cruises released their financials in preparation for an IPO.

I’m a bit obsessed with this business. Viking started in 1997 and has methodically built one of the best travel companies in the world - they have significant market share in the premium travel industry, they make good money, and they consistently grow way faster than their competitors.

If you want the backstory, check out my original piece. At the time I wrote that, it was clear they had built an amazing business but we could only observe it from the outside. Now, we have the chance to really understand the details and… they’re as impressive as they looked. The full F-1 filing is 200+ pages 😲. I read it so you don’t have to. Here we go…

Viking’s 2023 Financials

💵 Revenue: $4.7 billion

💵 Gross Margin: $1.6 billion (35% of revenue)

💵 Operating income: $818 million (17% of revenue)

💵 Net income: -$1.9 billion (a loss!? Explanation below 👇)

💵 Total Debt: $5.4 billion

💵 Cash: $1.5 billion

💵 ROIC: 27% (vs <10% for other public cruise companies)

This is a healthy business, especially for being so capital-intensive (27% ROIC!).

But what about that net income loss? It was driven by a $2 billion “Private Placement Derivatives” loss. That’s a non-operating, non-cash loss related to fair value accounting. It’s not relevant for understanding the performance of the business, but it does affect the current owners. Most importantly, it will go away once private shareholders’ equity is converted to public stock.

Operating and Per Passenger Statistics

🧑🤝🧑 Passengers Carried: 650,000

📈 Occupancy: 93.7% (95% river, 93% ocean)

🚢 Vessels: 92

🗓️ Avg. Booking Window: 11 months

🎟️ Revenue per passenger: $7,251

💲Total Revenue per APCD: $727 (APCD = available passenger cruise day)

💲Net Yield per APCD: $474 (net of commissions, air, & hotel expenses)

💲Gross Margin per APCD: $253 (net of commissions & operating expenses)

Note that river occupancy does not account for the 3-4 months that a river ship is out of service (usually in Q1). That said, the ocean ships operate year-round and have similarly high occupancy.

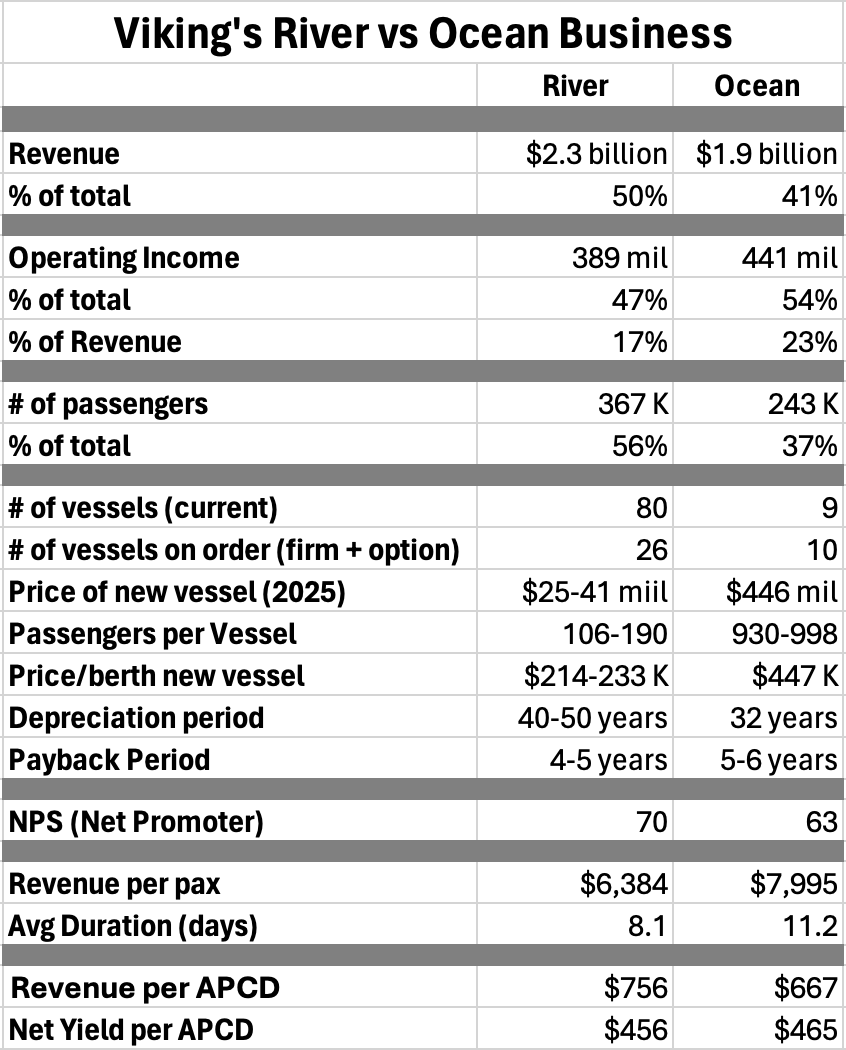

Comparing the River and Ocean business

Viking breaks out their two core segments: English-speaking ocean and river cruises (except Mississippi).1

A few takeaways:

River vessels have different economics than oceangoing ships. The price per berth of a river vessel is half of an ocean ship ($215-233 K vs $447K). The payback period is a year shorter than an ocean ship. Most river vessels operate 8-9 months whereas ocean ships operate year-round, contributing to the narrower difference in payback period. Lastly, because they operate in freshwater, river vessels have a useful life of 40-50 years, 10-18 years longer than ocean ships, which are exposed to corrosive saltwater.

River remains Viking’s largest product line, despite significant growth in ocean. 50% of revenues and 56% of passengers come from the river segment.

The Ocean unit is more profitable, generating 23% operating income vs 17% for the River division.

The Ocean unit will grow more aggressively in the next few years (66% vs 33% through 2028), likely driven by higher profitability and bigger potential – there are only so many European rivers. If you look at the full orderbook through 2030, the Ocean fleet doubles while the River vessels on order represent a 33% increase. Keep in mind: ocean shipbuilding slots are hot commodities, so Viking needs to reserve slots further in advance. It will be easier for Viking to supplement their river capacity on shorter notice.

Net Yield, which nets out commissions and pre/post flights + hotels, is about even between ocean and river. However, total Revenue is almost $89 (13%) higher for river. That implies either 1) a higher proportion of river products are commissioned trips sold through travel agents and/or 2) a higher proportion of river products are sold with bundled hotels and flights.

The average duration of an ocean cruise (11.2 days) is 3 days longer than a river cruise (8.1 days), which drives a higher average price for ocean cruises.

Growth

No matter how you cut it, Viking’s growth is impressive. In 2023, the cruise industry carried 11.4% more passengers than in 2017. In that same period, Viking grew their capacity 11.4% per year!

Revenue grew even faster than capacity, at 16.2% per year. That’s amazing. Normally, you’d expect some softness in price as a brand’s sales & marketing “machine” adjusted to filling so much new capacity. Viking grew capacity way above the industry norm, and they simultaneously increased price 🤯.

Another stat: their forward booked position is actually better now than it was in 2017.

For the 2017 season, 63.7% of Capacity PCDs for our core products were booked as of December 31, 2016, which increased to 73.9% of Capacity PCDs for our core products booked for the 2024 season as of December 31, 2023.

Going forward, Viking plans to grow in three ways:

First, they’ll continue to build capacity in their core ocean and river segments. They have firm orders and options for 36 vessels through 2030, and I suspect they’ll add more (they claim their core 55+ market is underserved 😄).

Second, they’ll expand the “platforms” they operate for their core 55+ English-speaking demographic. In the filing, they mention safaris and land tours as possibilities. Viking has demonstrated their ability to de-risk expansion by carry over their existing customer base to new platforms. 60% of the bookings in the first season of a new product (Viking Ocean, Expedition, Mississippi) were made by past guests, higher than the 50% they achieved overall in 2023.

As our guests generally enjoy multiple forms of travel and take multiple trips per year, land-based product offerings would meet an additional portion of the travel needs of our core demographic. This would enable us to capture a greater share of our guests’ travel spend and extend our customer lifetime value and connection to the Viking brand.

Third, Viking will expand outside their English-speaking core, to places “such as China and elsewhere in Asia, where we see significant growth potential.” Viking’s China efforts were stalled by Covid, but there’s clearly long-term potential. I’ve also seen ads on LinkedIn for Japanese-language crew, so I assume Japan is on the radar.

Viking approaches new demographics differently than other cruise companies. Most brands hunt for incremental demand in many countries, adding announcements and written materials in a new language. Vikings allocates vessels to one market at a time. Single-language ships ensure the Chinese (or Japanese?) experience is as high-quality as the core product, and the English-language product is not diluted by trying to do too much (like annoying multi-language announcements).

Core Demographic

US-heavy - In 2023, 90.5% of guests were from North America, 4.3% from the UK, and 5.2% from the rest of the world.

Clear definition - Viking defines their core demographic as “curious, affluent, English-speaking travelers aged 55 years and older”.

Focus - While other cruise companies appeal to a variety of consumers, Viking repeatedly emphasizes their focus on this core demographic, which they claim is underserved.

Growth - In the US, people 55+ make up 30% of the population, hold over 70% of the wealth, and they’re the fastest growing demographic. They also have the most time to go on vacations.

While Viking is looking at expanding beyond this core English-speaking demographic, I suspect they’ll aim for other “attractive demographics” - large, growing groups that merit investment.

Loyalty & Product Quality

Travel brands live and die by consumer loyalty. They spend hundreds or even thousands of dollars to acquire a customer. How many times will they come back?

Viking’s quality, focus on a core demographic, and regular introductions of new products have created customers that keep coming back

A few proof points:

Quality: On a 4 point scale, the average guest quality rating was 3.7 (70% of guests complete onboard surveys). Viking also consistently wins industry quality awards.

NPS: The Net Promoter Scores were 70 for Viking River and 63 for Viking Ocean in 2023.

Repeat rate: 51% of guests in 2023 had previously been on a Viking cruise

Booking Onboard: 18% of guests booked their next cruise while they were still onboard! This only applies to Ocean & Expedition guests. I assume river vessels don’t have an onboard sales person, so they’re excluded.

Distribution: Viking’s Major Advantage

Viking’s distribution - their “sales & marketing machine” – may be the best of any large travel company. It’s certainly better than any large cruise brand.

The main points…

Viking has a single brand. Many travel companies, including the publicly-traded cruise companies, have a portfolio of brands. That dilutes the power of brand advertising and it limits which products can be promoted to repeat guests (if I like Oceania, will I also like Regent?). Viking’s brand awareness is shockingly high - 71% unaided awareness for river cruises among their core demographic!

Viking spends big on marketing. Since their founding in 1997, they’ve spent $2.8 billion, most of it direct marketing. Their marketing database includes 56 million households in North American, of which 1.5 million are past guests.

On the brand side, they sponsor highbrow cultural content and events that appeal to their demographic. For example, they started sponsoring PBS Masterpiece Theater at the height of Downtown Abbey’s popularity and today, they sponsor the Los Angeles Philharmonic.

In 2023, more than 50% of bookings were made directly with the company (online or by phone). While Viking still relies heavily on travel agents for half their bookings, their proportion of direct bookings Is high for a luxury cruise brand of their size.

All of this contributes to impressive forward bookings:

We have a proven track record of selling Capacity PCDs well in advance of sailing. […] We grew Capacity PCDs for our core products from 3.3 million in 2017 to 6.7 million in 2024, a CAGR of 10.6%. Even with this growth, we continue to enter every season with a high percentage of Capacity PCDs booked. For the 2017 season, 63.7% of Capacity PCDs for our core products were booked as of December 31, 2016, which increased to 73.9% of Capacity PCDs for our core products booked for the 2024 season as of December 31, 2023. Entering a season with over 70% of Capacity PCDs sold provides significant revenue visibility, allowing us to focus our marketing efforts on selling future seasons earlier than competitors and continuing the cycle of strong Advance Bookings.

A few last tidbits

Consumer Insights - The filing makes repeated references to a “robust consumer insights” practice, which drives marketing decisions AND product decisions. Viking has fewer unique products than their competitors (fewer ship types and itineraries), which makes it worthwhile to invest in the the few products they do release.

Better Parking Spots - Viking promotes their docking locations – “ premium docking locations in Paris […] 800 meters from the Eiffel Tower, and in Luxor, Egypt at the Karnak Temple” – but I’ve never seen the details. Now we have them: “We control 67 premier docking locations for our river vessels along the rivers of Europe and Egypt and have priority access to 30 docking locations in Hungary.”

Longship Design vs Competitors - Viking has long boasted of the efficient design of their river vessels – we accommodate 190 passengers while the other guys accommodate 164 - but I’d never seen a diagram that showed how.

Thank you for reading! And thanks to Koushaw and Blake for explaining the financials.

The remaining “other” products are not broken out, but they include expedition (2 ships), Mississippi River (1 vessel), and China-related endeavors (1 ship in China, and a few Chinese-language river vessels in Europe).

Omg thank you for unpacking this. Lol. I really didn't want to read all 200+ pages. With all the disclaimers that you aren't a financial guy, yada yada yada... Are you leaning toward our against buying into the IPO?